Oil Is Faltering. Renewables Will Survive Trump. What Is Carney's Next Move?

Rising renewable energy investment plus unsteady oil prices may mean we're witnessing the last stand for fossil fuel expansion. With Alberta doubling down, how will Canada respond?

You wouldn’t know it from scanning through your daily dose of morning headlines, but we’re witnessing the beginning of the end of oil and gas.

And industry executives know it, even if they can’t or won’t say it out loud.

It won’t happen overnight. It remains to be seen whether we’ll rid ourselves of fossil fuels in time to hold off the worst impacts of climate change.

But when Canada’s oil sands and pipeline titans tout a new generation of fossil fuel infrastructure… when Donald Trump tries to command industry action, “and I mean NOW!!!”, on his “Drill, Baby, Drill” agenda… they’re pushing against two realities that are beyond their control:

• Weak fossil fuel demand is driving down the oil and gas prices on which the industry’s profits rise or fall. We’ll see those prices spike from time to time for the foreseeable future, but they won’t run high enough for long enough to pay for the multi-billion-dollar megaprojects the industry is promoting.

• The cheapest, quickest, most reliable way to meet new energy demand is with renewable sources like solar and wind, energy storage, and energy efficiency. Particularly smaller, decentralized sources that can be matched to local needs and help communities and businesses build resilience against the next local heatwave, flood, or power outage.

None of this will be enough to hold average global warming to 1.5°C without some potentially calamitous overshoot. As Environmental Funders Canada Executive Director Devika Shah pointed out recently on LinkedIn, lifelong champions like David Suzuki have “earned the right” to declare emission reductions a failure.

But the knowledge that every one-tenth of a degree of warming matters, that every increment of climate change prevented or permitted is measured in lives saved or lost, is pretty much as old as the 1.5°C target itself. So the worse things get, the more important it is to remember that the tide is beginning to turn, even if it’s taking longer and running into more sidetracks and unforced errors than any of us could have imagined.

Oil Is Over, Oil Analysts Say

You won’t hear this anytime soon from the oil and gas lobby, or from the agencies that report to their former hired hand in the Alberta premier’s office. But if you watch what the industry is doing and how its investors are responding, you can see that the die is cast.

Particularly when the news comes from some of the most staid, industry-focused voices on the planet.

“The world’s largest oil companies have endured a lost decade in the stock market, struggling to convince investors they can grow in a world where demand for their main product is expected to peak in the coming years.” the Financial Times reported in mid-June, citing a conclusion the International Energy Agency first published in May 2021.

“Oil majors are no strangers to boom-and-bust cycles,” the Times added. “But now the challenge may be structural. The rapid adoption of electric vehicles, especially in China, has surprised the industry. Many oil majors now concede that their production will probably peak within the next decade”. So colossal fossils like ExxonMobil, Shell, BP, and Norway’s Equinor are now working to “squeeze every molecule”, in the words of Equinor CEO Anders Opedal, before the music stops.

Equinor isn’t alone. Every fossil company everywhere wants investors, governments, and citizens to think, even against the thinnest of evidence, it will be the last one standing as its business steadily crashes. But times are already tough, and the tell comes from two of the industry’s biggest voices: a branch of the U.S. Federal Reserve, and the world’s oil and gas cartel.

An Oil Price Crash This Year?

The Federal Reserve Bank of Dallas is the branch of the U.S. central banking system that reports on the economy of Texas and the southwestern part of the country, “particularly energy research,” Investopedia explains. Despite Trump promising, then demanding, a new golden age for oil and gas drillers, the Dallas Fed sees industry activity falling slightly amid import tariffs, lower oil prices, and—significantly, finally—concerns about "whether produced water management could constrain drilling and completion activity in the Permian Basin.”

That’s bank-speak for the recognition that oil and gas fracking consumes and pollutes obscene volumes of water in a region where a continuing mega-drought has reduced parts of the mighty Colorado River to a trickle.

Overall, the Dallas Fed’s survey of 136 oil and gas companies in late June found business activity declining, uncertainty rising, production down, and employment falling slightly—all in sharp contrast to the bullish optimism you hear whenever a fossil exec gets anywhere near a microphone.

“Perhaps more pressing for oil and gas executives is the price of oil itself,” the Journal of Petroleum Technology writes in its summary of the survey. “If prices fall to an average of $60/barrel over the next 12 months, two-thirds of the 85 oil and gas executives who responded to the question said they would reduce production. If prices drop to $50/barrel, 88% said they would cut production either slightly or significantly.”

Prices are already a problem for the industry, even as the surge in data centres and artificial intelligence drives a rapid rise in electricity demand.

“Right now, oil prices are at four-year lows and natural gas prices are falling, and when prices are low, it’s much harder to make the business case for more mining, drilling, and power plants, even with incentives,” Vox reported last week. “Trump may have some levers to pull—he can, for example, open up more federally managed lands for energy production—but many of those leases sit unused because energy companies don’t want to create a supply glut.”

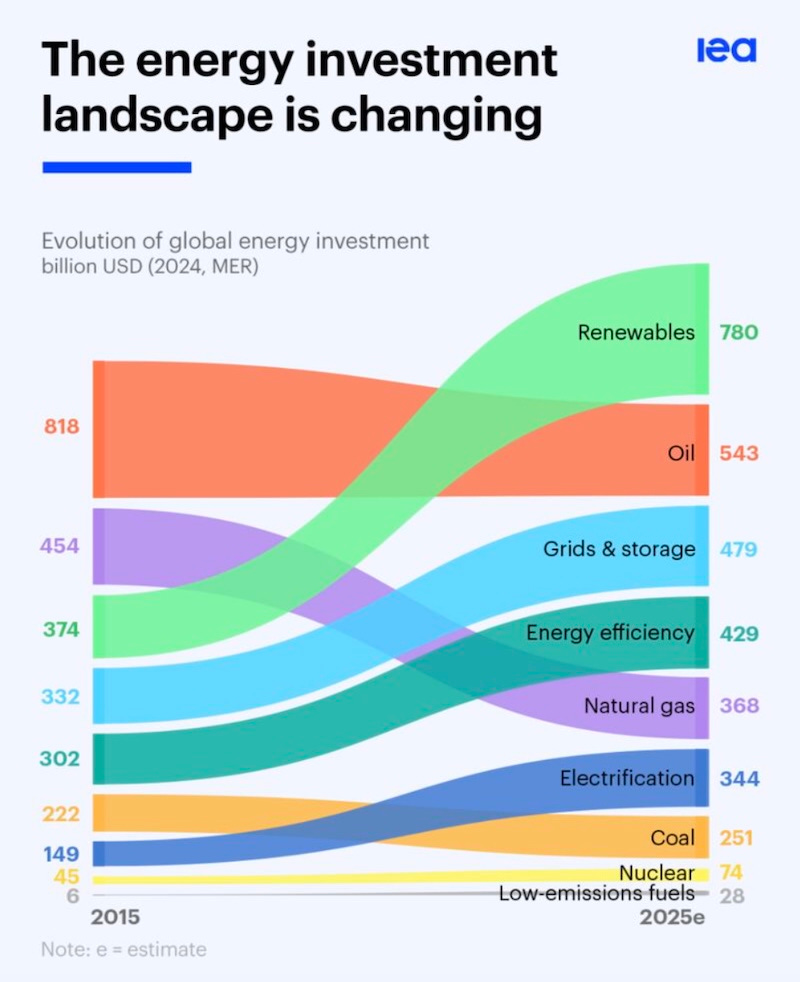

Instead, investors’ attention is shifting to options that can actually deliver the power they need, when and where they need it—which increasingly means non-fossil sources that also bring down emissions. Despite the worst obstacles Trump can throw in its path, clean energy investment is expected to hit $2.2 trillion this year, double the amount still pouring into fossil fuels, the International Energy Agency reported last month, and there’s a school of thought that the U.S. rollbacks have created a perfect opportunity to invest in renewables now for future gain.

“We’re in this moment of surging demand and you can’t build another gas turbine for at least five years beyond what’s already been booked,” Robbie Orvis, senior director for modelling and analysis at the Energy Innovation think tank, told Vox. “We have this demand growth that’s going to have to be met. The only thing you can build to meet it on the timeline needed over the next five to 10 years is solar, wind, or battery storage.”

It doesn’t help the fossil industry’s case that the Organization of the Petroleum Exporting Countries and its allies (OPEC+) have chosen this moment to challenge U.S. dominance of global oil and gas markets.

“OPEC+ will increase production again next month as the Saudi Arabia-led oil cartel seeks to win back market share in a move that is likely to put downward pressure on crude prices,” the Times reported over the weekend. “In the longer term, the increase in production threatens to add to what most traders expect to be a significant supply surplus by the end of the year that may push prices to below $60 a barrel”—the magic threshold where two-thirds of U.S. oil drillers said they would cut production.

Will We All Have to Pick Up the Tab?

A decline for oil and gas is obvious good news for the energy transition. It will rattle fossil fuel investors and impair companies’ ability to open up new exploration sites. Eventually, it will erode the political and public clout of the industry that first understood the climate emergency in the 1970s, but chose to spend decades financing climate denial rather than letting the rest of us in on the secret.

The problem is that citizens, rather than fossil companies and their shareholders, might be stuck picking up the tab.

"Too many oil and gas companies are betting on demand that won't materialize in a decarbonizing world, and the public are at risk of paying the bill," James Alexander, CEO of the UK Sustainable Investment and Finance Association (UKSIF), told Bloomberg.

Alexander was commenting on a report by UKSIF and Transition Risk Exeter that said the energy transition could lead to $2.3 trillion in stranded assets by the end of this decade as fossil projects “lose economic viability” before the end of their expected operating lives.

“Though vast, those losses are considerably smaller than the economic destruction that would follow if the world abandons its efforts to slash greenhouse gas emissions,” Bloomberg writes, citing the report.

Which Way Will Canada Tip?

None of this is news to Prime Minister Mark Carney, who previously took “a very strong line” against banks investing in fossil fuel projects destined to become stranded assets, Sir David King, the former chief scientific advisor to the UK government, told The Energy Mix a couple of weeks ago. “He understands the risks of climate change. He doesn’t need a lecture on this issue.”

The problem is that Carney’s new government has been distinctly, probably deliberately vague on that point, and will likely continue down that road until the fall. So we see Natural Resources Minister Tim Hodgson hinting that the government could consider scrapping regulatory cornerstones like the federal oil and gas emissions cap, the Impact Assessment Act, and clean electricity regulations “over time”. In virtually the same organizational breath, Environment and Climate Minister Julie Dabrusin insists that essential protections will remain.

A big part of the problem is that so many Canadian investors—investors we can expect Carney to listen to avidly—are still hooked on oil.

“The big challenge for the Carney government—and for Canada—is to get our banks and other financial institutions to think beyond pipelines to new sources of economic growth, based on ideas, intangibles, and intellectual property,” writes the Toronto Star’s former economics editor David Crane, in a post for The Hill Times. But those institutions “see our future as a raw material or commodity producer serving the industrial needs of the United States and other countries, without adding value.”

The financial sector’s failure to follow the evidence on climate change and the energy transition may partly explain a federal approach to “nation-building” projects that has raised alarm in many corners of the climate and energy community, though not all.

Canadian Climate Institute President Rick Smith told The Hill Times it’s still “early days” and “too early to tell” where Carney will land in a choice between fossil fuel infrastructure and sound climate policy. But “the Liberal platform held promise, with a ‘specific’ and ‘fact-based’ approach that made clear Carney’s position on the ‘necessity of aligning a good climate policy and good economics’,” the Times writes, citing Smith.

“There has been no more eloquent person on the topic of the importance of good, smart, effective climate policy when it comes to building economic prosperity than the prime minister,” Smith said.

Pembina Institute Executive Director Chris Severson-Baker said Carney’s controversial One Canadian Economy Act has “raised a lot of concern”. But “what I take a bit of comfort in is the fact that … a lot of the things we need in order to reduce emissions in our economies are now more economically viable than… maintaining the status quo,” he told the Times.

The Fossil Industry’s Last Stand

The industry and its backers clearly see that potential, too. And they’ve been panicking about it, in a flurry of opinion pieces that home in on Carney’s past climate credentials and demand a complete capitulation to Alberta’s deregulatory agenda.

But sometimes when we panic, we make mistakes—deliberately or not. When retired pipeline executive Dennis McConaghy took to the pages of the Calgary Herald July 5, he admitted that none of the low-carbon spin we’ve been hearing from the oil sands industry has an ounce of substance.

Emission caps are essentially production caps. No invocation of unaffordable carbon capture technology can materially alter that. As for buying domestic or international offsets, even assuming availability, it would impose costs that Canadian hydrocarbon producers’ global competitors don’t choose to impose on themselves.

So what do you do if you’re an industry that lies through its teeth, routinely breaks its promises, sees it emissions rise 143% over an 18-year span while the rest of the country begins to decarbonize, then demands huge regulatory breaks and lavish taxpayer subsidies to carry on as usual in the midst of a climate emergency?

Simple. You double down, of course.

“If Alberta cannot gain these concessions, then what?” McConaghy thunders. “No concessions should mean no delusions by Albertans—this Carney government is not aligned with Alberta’s fundamental economic interests. Facing such treatment, Albertans deserve an immediate democratic means to express themselves, even if fundamental political change hangs in the balance.”

It's an easy out, but solves nothing, to reflexively blame and vilify Ottawa when the foundations that support your industry are beginning to crumble before your eyes—and when the real attack on the province’s economic future is coming from within. And it’s nothing new. Nearly a decade ago, fossil execs and their financiers said they were losing patience with the federal government. Warning of a new wave of western Canadian separatism. Accusing-not accusing Ottawa of treason.

And in that round, another Albertan got it right.

“We can’t control the world price of oil,” then-Calgary mayor Naheed Nenshi acknowledged in a talk to the Ottawa Mayors’ Breakfast in 2016.. “Many people in Alberta seem to think [then premier Rachel] Notley sets it every morning. She doesn’t. The Prime Minister does.”

Nenshi was kidding, of course, and the comment got a good laugh. A decade later, the problem is that no one is getting the joke, and its real-world impact is now a lot closer to hitting the industry and the province full force.

Mitchell Beer traces his background in renewable energy and energy efficiency back to 1977, in climate change to 1997. Now he and the rest of the Energy Mix team scan 1,200 news headlines a week to pull together The Energy Mix, The Energy Mix Weekender, and our weekly feature digests, Cities & Communities and Heat & Power.

Chart of the Week

‘Blatant Political Capture’ Feared as Saudi Aramco Economist Nominated to Lead IPCC Science Role

Berlin Court Allows Referendum on Car-Free City Centre

What Wildfire Emissions Mean for Canada’s Climate Progress

Alberta Removes Emissions Ceiling as Gas Flaring Hits New High

Canada’s LNG Touted—And Doubted—as ‘Transition’ Fuel as Doctors Sound the Alarm

Data Centres Tap Into Wasted Renewable Electricity

Canada Signs On as Co-Convener of Global Methane Pledge

16,386 Consecutive Days of Petrochemical Pollution Land Exxon with Record Fine

LOST IN SPACE: Pioneering Methane Monitoring Satellite Shuts Down, Is ‘Likely Not Recoverable’

'Absolutely horrendous day' in Tataskweyak Cree Nation as wildfire destroys at least 7 homes (Canadian Broadcasting Corporation)

Asia warming nearly twice as fast as the global average, wreaking a heavy toll on the region’s economies (Times of India)

Recent droughts are 'slow-moving global catastrophe' - UN report (British Broadcasting Corporation)

Amid Brutal Heat Wave, Officials Stress Health Risks of Hot Nights (Inside Climate News)

A Special ‘Climate’ Visa? People in Tuvalu Are Applying Fast. (New York Times)

Ontario environment minister said 'we are on track' to meet 2030 climate targets. Internal docs disagree (Canadian Broadcasting Corporation)

Trump’s green-bashing is precisely why it’s a good time to buy green (Globe and Mail)

World’s largest sand battery commissioned in Finland (Balkan Green Energy News)

How plug-in balcony solar panels could help Britons save 30% on energy bills (The Independent)

New Handbook Aims to Protect Scientists From Autocratic Threats (Inside Climate News)

Private jet carbon emissions are soaring. Here’s who pollutes the most. (Washington Post)

Sabotage suspected as mystery blasts hit oil tankers (The Financial Times)

I wonder if your assessment might come into conflict with the thesis in “The Price is Wrong” by Brett Christopers? Tyler Swanson’s summary of his book states: "Viewing the energy transition and the development of renewable energy through the prism of price is misleading because, economically, price is not the problem. Rather, the issue is that renewables are not profitable enough relative to other forms of energy, and government support is necessary to make the profitability of renewables both visible and viable.” This is a great summary of his point that finance will continue to support oil and gas despite the price, and is this the same for government? Why government still subsidizes oil and gas far in excess of renewables has always been a mystery to me and I think Brett’s book explains it.